This Should Be a Bright – If Bumpy – Year for Stocks

January 11, 2021

While 2021 will likely be a positive year for equities, the longer-term outlook is clouded by the potential for higher taxes, higher interest rates and lower valuations. Hear more from Mike Gibbs, managing director, and Joey Madere, CFA, senior portfolio analyst, both of the Equity Portfolio & Technical Strategy group.

To read the full article, see the Investment Strategy Quarterly publication linked below.

We maintain a positive view for equity markets in 2021. This stance stems from our expectation for an economic recovery, fueled by the likelihood of at least three vaccines with stated 90%+ efficacy rates. Economic data and corporate earnings have recovered well above expectations from six to nine months ago, momentum that we believe will continue over the intermediate term. We also believe the Federal Reserve (Fed) will remain accommodative and ready to support the economic recovery as needed.

The Democratic sweep raises the odds of higher fiscal stimulus and spending; however, it’s also likely that Democrats will want to pay for this stimulus with higher taxes down the road. The slim majority may temper the ability for the full agenda to be completed and may make the battles tougher, but we do believe the majority of President-elect Joe Biden’s agenda ultimately gets accomplished. The result is a net positive for potential economic growth this year, and consequently enhances the reflation trade already underway on vaccine optimism.

However, while the short-term outlook (6-12 months) is bolstered due to the likelihood of increased stimulus, the longer-term outlook is murkier given the potential for higher taxes, higher interest rates and lower valuations. The prospect of higher taxes will likely be a headwind to earnings growth in 2022 and 2023. It will also likely be a headwind to valuation multiples later this year as investors position themselves over time for the coming changes.

Additionally, questions remain about the ongoing virus surge, vaccine capacity and distribution, timing and size of stimulus and the pace of the economic recovery. So while we’re positive on equities over the next 12 months, we wouldn’t be surprised if the road is bumpy along the way.

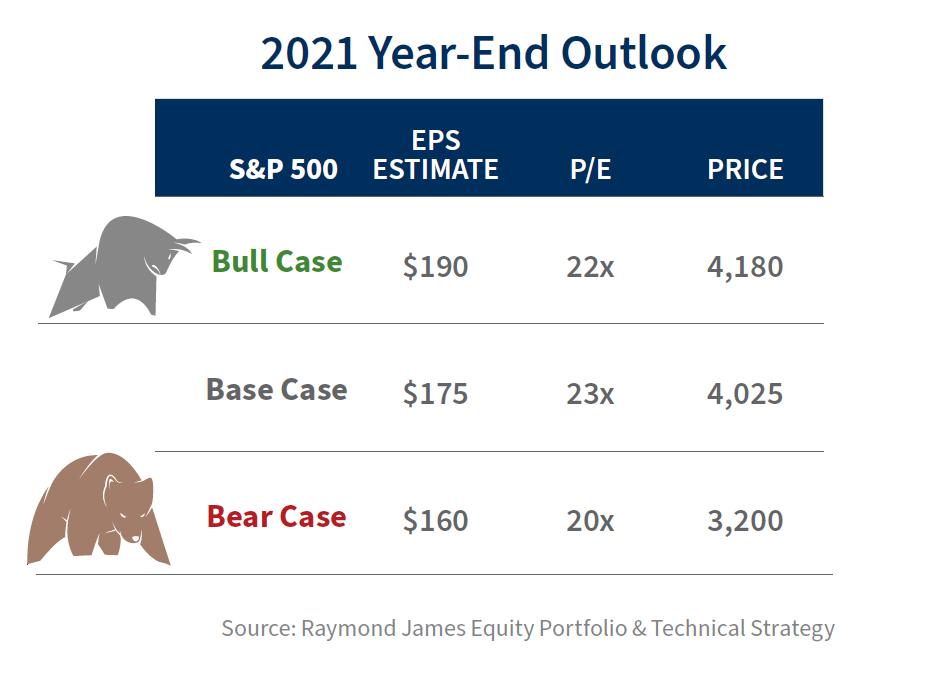

S&P 500 base case: 4,025

Our base case S&P 500 target for 2021 is 4,025, representing $175 earnings per share (EPS) and a 23x price-to-earnings (P/E) ratio. We use $175 in earnings, above the current consensus estimate of $166, due to our positive expectation for economic and fundamental recovery in the year ahead. It’s also normal for estimates to be revised higher coming out of recessions, as analysts historically set the bar too low in dire economic times. Earnings estimates for 2021 have been revised higher by 4% so far, and our estimate of $175 reflects just a 4.5% further move upward. This $175 estimate is a 27% snap-back in growth from 2020’s pandemic-depressed earnings and 9% above 2019 earnings.

We also believe valuation multiples can remain elevated given the low inflationary and interest rate environment. The current S&P 500 P/E of 27.5x is well above the historical average of 16.5x. However, when taken in conjunction with still low-interest rates, the current valuation is more reasonable. The equity risk premium (S&P 500 earnings yield vs. U.S. 10-year Treasury yield) is currently 2.6%, well above its long-term average of 0.6% (since 1954) and just marginally below its pre-pandemic level last January. Moreover, the S&P 500 dividend yield of 1.5% is 0.5% higher than the U.S. 10-year Treasury yield. Despite equities being at all-time highs, this is still in line with the highest spreads on record prior to COVID-19 – reflecting a still-attractive environment for equities versus bonds.

It is also normal for valuations to elevate coming out of recessions due to depressed earnings as investors discount the eventual recovery. As earnings rebound in 2021, we expect the S&P 500 P/E multiple to contract. However, the Fed has stated its intent to keep interest rates lower for longer in order to support the economic recovery, which also supports above-average multiples in our view. Therefore, we use a 23x P/E in our base case 2021 scenario which, combined with our $175 earnings estimate, produces a S&P 500 target of 4,025.

S&P 500 bull case: 4,180

In the event that the virus spread subsides and COVID-19 vaccinations allow a quicker reopening process (in conjunction with fiscal stimulus) that results in upside to growth expectations throughout 2021 (i.e., GDP growth is closer to ~6.5% than ~4.5%), we believe S&P 500 earnings could potentially reach $190. With this stronger growth backdrop, it is likely that inflation and interest rates are marginally higher than under our base case scenario, resulting in a slightly lower valuation assumption. We use a 22x P/E in this scenario as valuation also normalizes at a quicker rate. Applying this 22x P/E to $190 earnings results in a bull case S&P 500 target of 4,180.

S&P 500 bear case: 3,200

If virus concerns linger for longer and hamper the reopening process and pace of economic recovery (i.e., GDP growth is closer to 3% in 2021), we believe earnings revisions could break from their historical upward trend out of recessions and finish near $160. In this scenario, tax increases also become an overarching theme for the longer-term outlook and outweigh the benefits of spending increases. As investors discount the impact from these tax changes to 2022 earnings, the result is a lower P/E. We use a 20x P/E (which is over 10% lower than our base case P/E assumption of 23x) in this scenario, resulting in a S&P 500 bear case target of 3,200.

Read the full Investment Strategy Quarterly

All investments are subject to risk, including loss. Past performance may not be indicative of future results. The performance noted does not include fees and charges which an investor would incur. Investing in international securities involves additional risks such as currency fluctuations, differing financial accounting standards, and possible political and economic instability. These risks are greater in emerging markets. Small cap securities generally involve greater risks and are not suitable for all investors. Companies engaged in businesses related to a specific sector are subject to fierce competition does not guarantee a profit nor protect against loss. Dividends are not guaranteed and will fluctuate.