Year-End Portfolio Rebalancing

Drew O’Neil discusses fixed income market conditions and offers insight for bond investors.

Your investment portfolio likely has some sort of target asset allocation designed to align your financial goals with an appropriate level of risk. Allocation targets are intended to balance various risks while working toward longer term objectives by targeting a certain percentage of your portfolio to be invested in various asset classes. While there are a wide range of potential asset classes for investors to choose from, this commentary will focus on the two primary categories that make up many investors’ portfolios: equities and fixed income. Equities are often the product of choice used for capital growth (total return) while fixed income is oftentimes earmarked with the primary purpose of capital preservation. The known maturity date, known maturity price, and known stream of cash flows that come with owning bonds provide the qualities that help to preserve wealth*.

An important part of ensuring that portfolio allocation remains within an investor’s risk tolerance is rebalancing assets periodically to make sure that market performance doesn’t pull portfolio allocations too far out of line from targets. In a year where equities outperform fixed income, portfolio rebalancing accomplishes taking some of the wealth that was created on the equity side of the portfolio and moving it over to the fixed income side of the portfolio in order to preserve the newly created wealth. The strong 2021 year-to-date stock market performance has likely pushed many investors away from their target portfolio allocations.

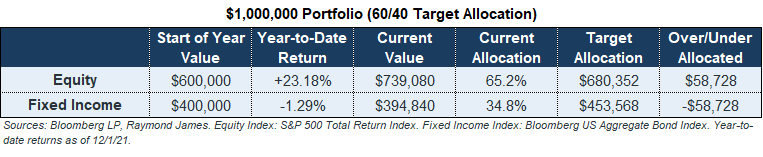

The chart below illustrates a simple example where an investor started out the year with a $1,000,000 portfolio allocated in line with their targets, with 60% in equities and 40% in fixed income. Using the S&P 500 Total Return Index as a proxy for equities and the US Aggregate Bond Index as a proxy for fixed income, this investor would currently be under-allocated to the capital preservation portion of their portfolio (fixed income) to the tune of nearly $60,000. Simply put: this investor currently has a riskier portfolio than they are targeting. Year-end rebalancing would dictate moving ~$60,000 out of equities and into fixing income in order to move back into alignment.

As we approach the end of the year with an eye on 2022, now is a good time to take a fresh look at your portfolio with your financial advisor and assess whether or not your current asset allocation aligns with your intended targets, long-term goals, and risk tolerance. Regardless of interest rate levels, fixed income’s unique attributes make it an ideal investment for wealth preservation. Keep in mind that when buying individual bonds and holding them to maturity, market performance does not affect when and how much wealth is returned to you*.

Another thing to keep in mind as you are rebalancing your portfolio, or anytime an investment is being sold, is the tax consequences of selling investments. Depending on the investor’s personal situation, losses can sometimes be “captured” in order to offset current or future capital gains. With this in mind, sometimes selling and repositioning within fixed income can be advantageous to the investor if there is an opportunity to capture losses, even when overall portfolio rebalancing does not dictate moving assets away from fixed income.

*Barring a default.

Raymond James is not a tax advisor. Please consult a tax professional prior to making any investment decisions.

To learn more about the risks and rewards of investing in fixed income, please access the Securities Industry and Financial Markets Association’s “Learn More” section of investinginbonds.com, FINRA’s “Smart Bond Investing” section of finra.org, and the Municipal Securities Rulemaking Board’s (MSRB) Electronic Municipal Market Access System (EMMA) “Education Center” section of emma.msrb.org.

The author of this material is a Trader in the Fixed Income Department of Raymond James & Associates (RJA), and is not an Analyst. Any opinions expressed may differ from opinions expressed by other departments of RJA, including our Equity Research Department, and are subject to change without notice. The data and information contained herein was obtained from sources considered to be reliable, but RJA does not guarantee its accuracy and/or completeness. Neither the information nor any opinions expressed constitute a solicitation for the purchase or sale of any security referred to herein. This material may include analysis of sectors, securities and/or derivatives that RJA may have positions, long or short, held proprietarily. RJA or its affiliates may execute transactions which may not be consistent with the report’s conclusions. RJA may also have performed investment banking services for the issuers of such securities. Investors should discuss the risks inherent in bonds with their Raymond James Financial Advisor. Risks include, but are not limited to, changes in interest rates, liquidity, credit quality, volatility, and duration. Past performance is no assurance of future results.

Stocks are appropriate for investors who have a more aggressive investment objective, since they fluctuate in value and involve risks including the possible loss of capital. Dividends will fluctuate and are not guaranteed. Prior to making an investment decision, please consult with your financial advisor about your individual situation.