Peak Inflation, So What?

Chief Economist Scott Brown discusses current economic conditions.

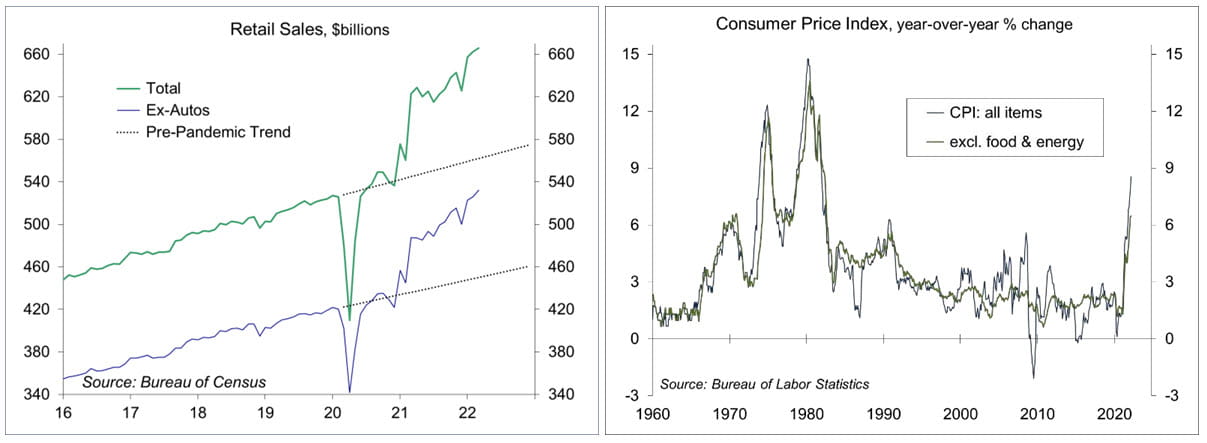

Higher gasoline prices (+18.3% m/m, +48.0% y/y) fueled a 1.2% increase in the Consumer Price Index in March, bringing the year-over-year gain to 8.5%. Food prices rose 1.0% (+8.8% y/y). Scary stuff. However, financial market participants took some encouragement from the downside surprise in the core CPI, which rose 0.3% (vs. expectations of +0.5%). Has inflation peaked? Very likely. However, the key question is how much of a decline we’ll see in inflation from here and whether the Fed will have to be more aggressive in raising short-term interest rate in the months ahead.

Prior to seasonal adjustment, retail gasoline prices rose 19.8%. Gasoline prices have fallen about 5% since mid-March. The CPI’s seasonal adjustment anticipates a 5.5% rise in April. Consequently, seasonally adjusted gasoline prices are poised to subtract 0.3 percentage points from the headline April CPI figure. A 0.6% m/m gain in April 2021 will roll off the back end of the year-over-year CPI increase. It’s very likely that headline inflation has peaked.

The price index for food at home rose 1.5% in March, following +1.0% in January and +1.4% in February, up 10.0% from a year ago – that’s not good. The price index for food away from home rose 0.3% (+6.9% y/y).

Ex-food & energy, the CPI rose 6.5% year-over-year. The mix has been unusual. The price index for durable goods fell 0.9% in March (+17.4% y/ y), largely reflecting a 3.8% decline in the index for used cars and trucks (which were still up 35.3% y/y). The price index for non-energy services rose 0.6% (+4.7% y/y), partly reflecting a 2.0% increase in transportation services (+7.7% y/y). Looking ahead, we can expect prices of consumer durable goods to slow and possibly decline somewhat, but durables account for just 13% of the CPI. Non-energy services account for 57.2% of the CPI – and the upward trend is a concern. Shelter costs (32.7% of the CPI), consisting largely of rent and rental equivalents, rose 0.5% in March, up 5.0% year-over-year. Other services are thought to be more reflective of labor costs. Heading toward the summer travel season, there’s a lot of pent-up demand. Consumers may complain about higher airfares and hotel fees, but they’ve been couped up for two years now, and will pay it. We are likely to get some relief in goods price inflation, but inflation in consumer services will be with us for a while. Hence, inflation should moderate, but remain relatively high in the near term.

Inflation is high outside the U.S. (7% in the U.K., 7.5% in the Euro Zone), so we can’t pin it entirely on U.S. economic policies. Elevated inflation reflects an imbalance between supply and demand. Following lockdowns in China and the Russian invasion of Ukraine, global supply chains are going to remain strained. The Fed can’t do much about supply, but it can tighten monetary policy to dampen demand. Strong growth is good, but the U.S. economy has been expanding beyond a long-term sustainable pace. We can see that in the falling unemployment rate and rising trade deficit. Monetary policy is currently far from neutral, let alone tight.

Retail sales rose 0.5% in the advance estimate for March (+6.9% y/y), with upward revisions to January and February, boosted by an 8.9% increase in gasoline sales (ex-gasoline, sales fell 0.3%). Ex-autos, building materials, and gasoline, sales edged up 0.1%, but up at an 11.9% annual rate for the quarter (vs. 4Q21).

The Consumer Price Index jumped 1.2% in March (+8.5% y/y), up 0.3% ex-food & energy (+6.5% y/y). The Trimmed-Mean CPI rose 0.5% (+6.1% y/y), indicating that inflation has broadened across categories.

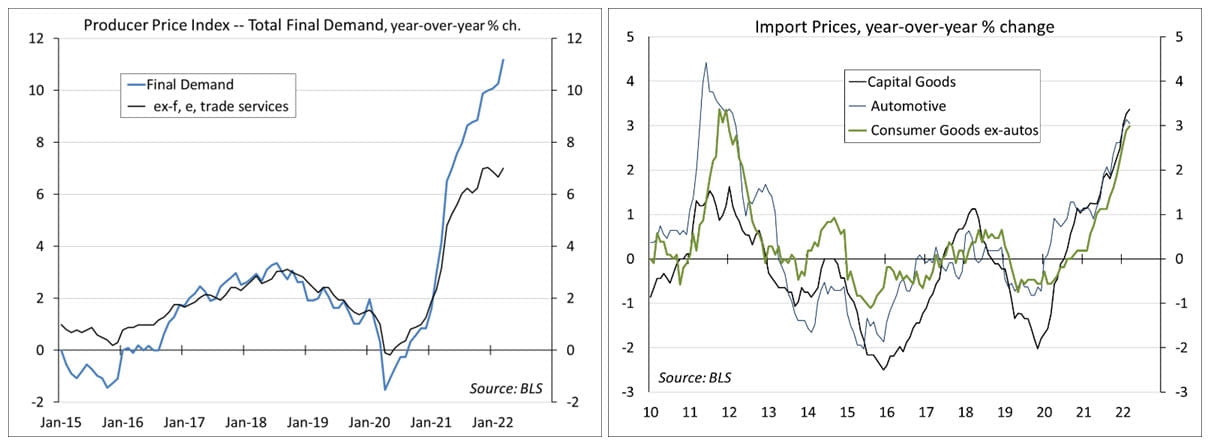

The Producer Price Index rose 1.4% in March (+11.2% y/y), up 0.9% ex-food, energy, and trade services.

Import prices rose 2.6% (+12.5% y/y) in the initial estimate for March, led by a 16.1% (+66.5% y/y) increase in petroleum. Price of imported raw materials remined elevated.

Jobless claims rose by 18,000 in the latest week, leaving the four-week average at 172,250 – a very low trend.

UM Consumer Sentiment rose to 65.7 in mid-April (the second lowest reading of the last decade), vs. 59.4 in March. Improvement was concentrated in expectations, reflecting the belief that gasoline prices have peaked. The survey ran from March 23 to April 12.

The opinions offered by Dr. Brown are provided as of the date above and subject to change. For more information about this report – to discuss how this outlook may affect your personal situation and/or to learn how this insight may be incorporated into your investment strategy – please contact your financial advisor or use the convenient Office Locator to find our office(s) nearest you today.

This material is being provided for informational purposes only. Any information should not be deemed a recommendation to buy, hold or sell any security. Certain information has been obtained from third-party sources we consider reliable, but we do not guarantee that such information is accurate or complete. This report is not a complete description of the securities, markets, or developments referred to in this material and does not include all available data necessary for making an investment decision. Prior to making an investment decision, please consult with your financial advisor about your individual situation. Investing involves risk and you may incur a profit or loss regardless of strategy selected. There is no guarantee that the statements, opinions or forecasts provided herein will prove to be correct.