Headwinds are building for the consumer

Review the latest Weekly Headings by CIO Larry Adam.

Key Takeaways

- Mild recession remains our base case

- Headwinds are building for the consumer

- Surging borrowing costs Pose a risk

This week we celebrated National Mulligan Day – a day everyone gets a ‘do over’ or a second chance. I’m sure there are plenty of golfers, weathermen, and others that have called for a mulligan every now and then. But unlike golfers, it is not often that economists are so far off in forecasting the timing of a recession. Yet this cycle, economists have been calling for a recession that, for two years, has yet to materialize. And that has many economists calling for a ‘mulligan’ with their forecasts, with a recession no longer the consensus forecast over the next 12 months. And with next week’s 3Q GDP report shaping up to be a blockbuster number (the Atlanta Fed GDPNow is tracking a +5.4% growth rate), it is worthwhile to reiterate our thoughts on the economy and how we expect growth to unfold over the next year.

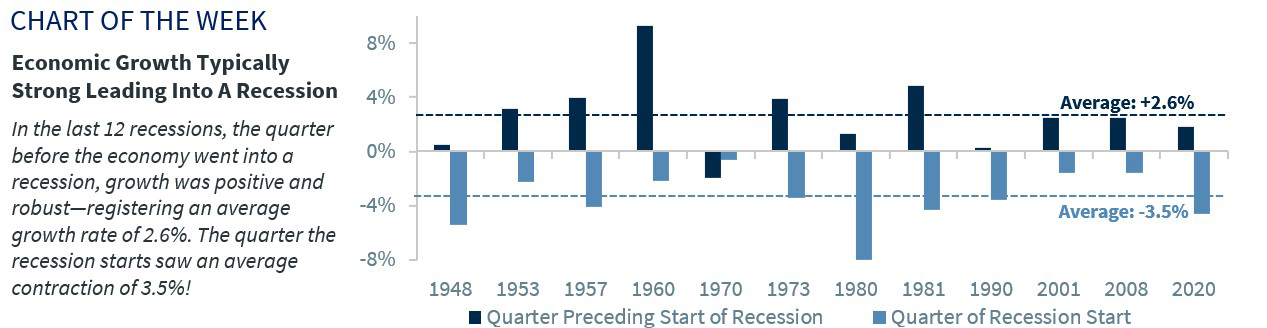

A mild Recession is still our base case | Economic activity continues to expand at a healthy pace, supported by a tight labor market and a resilient consumer. However, it is important to keep in mind that next week’s GDP report will reflect economic activity that occurred in the July through September period, a time when consumers were enjoying the Summer of Revenge Travel II. And while growth has been stronger than expected, it can turn around very quickly. In fact, history has shown that over the last twelve recessions, the quarter before the economy enters a recession has seen growth up, on average, 2.6%. And with the market so focused on binary outcomes – recession or no recession – it is missing the bigger picture. And that is: growth will be much slower over the next nine months and lead to a mild recession. Here’s why:

- Headwinds are building for the consumer | The tailwinds that have driven consumer spending since the pandemic have faded. Excess savings have essentially evaporated. Borrowing costs are at their highest level in decades. And student loan repayments, which resumed on October 1, are taking a bite out of disposable income. Sure, consumers have jobs and income right now, but their ability to continue to consume indiscriminately is coming to an end. In fact, this was echoed in this week’s earnings report by Bank of America’s CEO, Brian Moynihan, who commented that consumer spending has slowed considerably and is running at levels consistent with the low inflation, low growth economy that existed prior to the pandemic. Credit card usage is up significantly (now above $1T), suggesting that some consumers are having a harder time making ends meet. And judging by the recent delinquency data, more Americans are starting to fall behind on their debt obligations. While we are not suggesting that consumption is going to fall off a cliff, a moderation in spending should be expected.

- Surging borrowing costs pose a risk | The rapid rise in interest rates over the last few months will pose another threat to growth. With mortgage rates now above 8%, credit card rates at their highest level on record and small business borrowing costs nearing 10%, future spending and capex decisions are going to require a higher level of scrutiny. And with housing affordability now sitting at an all time low (and that is before the recent surge in interest rates!), residential real estate activity will likely remain frozen. This is starting to take a toll on home builder confidence again, which has fallen to its lowest level since January 2023. With more buyers getting priced out of the market and 30-year mortgage rates at a 23-year high, adjustable-rate mortgages (ARMs) are starting to make a comeback. These dynamics have pushed the share of ARMs on new loans to an 11-month high of over 9%. Business capex plans have also been impacted. In fact, a composite of regional Fed capex surveys shows that business capex spending plans over the next six months have fallen to their second lowest level in the post-COVID era.

- Falling confidence, strikes and a potential shutdown | Between higher interest rates, rising gas prices, a new war breaking out in the Middle East, and jittery financial markets, consumer sentiment is deteriorating again. In fact, the Conference Board’s Expectations Index, which reflects consumers attitudes about the short-term outlook for the economy, the jobs market and income prospects, tumbled to its lowest level in four months – a level that historically signals a recession within the next year (according to the Conference Board). And with the availability of credit constrained as bank’s tighten lending standards further and consumers become increasingly concerned about their financial outlook, a slowdown in consumer spending should start to materialize. As a result, all eyes will be watching consumer spending patterns heading into the crucial holiday shopping season. Early indications from a recent Gartner survey suggest that holiday spending will be softer this year, with only 9% of respondents expected to spend more on gifts. Add in the possible disruptions from the ongoing autoworkers strikes (which is in its fourth week) and a potential temporary federal government shutdown in mid-November, and growth could look considerably weaker in the months ahead.

All expressions of opinion reflect the judgment of the author(s) and the Investment Strategy Committee, and are subject to change. This information should not be construed as a recommendation. The foregoing content is subject to change at any time without notice. Content provided herein is for informational purposes only. There is no guarantee that these statements, opinions or forecasts provided herein will prove to be correct. Past performance is not a guarantee of future results. Indices and peer groups are not available for direct investment. Any investor who attempts to mimic the performance of an index or peer group would incur fees and expenses that would reduce returns. No investment strategy can guarantee success. Economic and market conditions are subject to change. Investing involves risks including the possible loss of capital.

The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. Diversification and asset allocation do not ensure a profit or protect against a loss.