Live by the numbers, die by the numbers

Chief Economist Eugenio J. Alemán discusses current economic conditions.

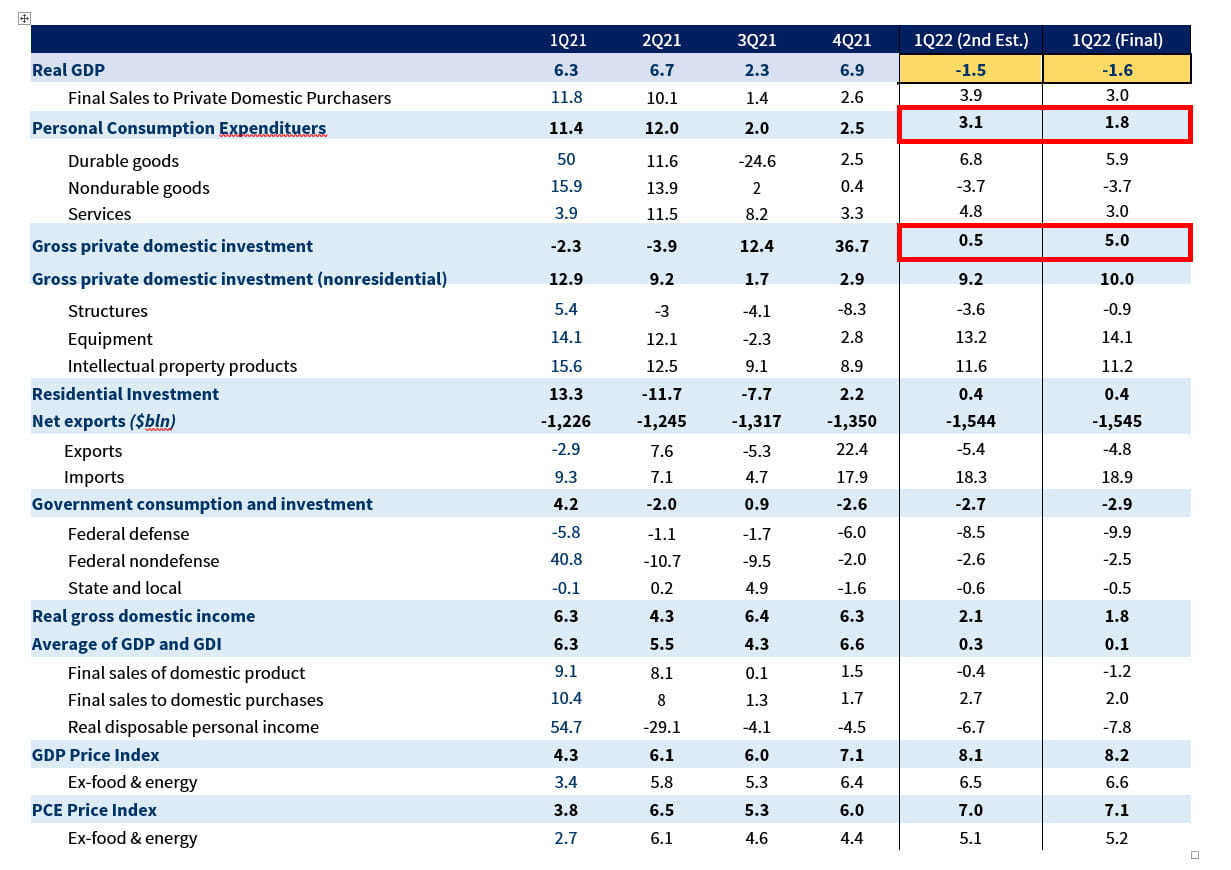

The third estimate for 2022 Q1 GDP from the Bureau of Economic Analysis was a real shocker. It was a shocker not only because it was released a day before the end of the second quarter or because it was revised further down to -1.7% from the second estimate of -1.6%. It was a shocker because of the large downward revision made to the growth in personal consumption expenditures (PCE) and the large upward revision to the growth in gross private domestic investment (GPDI). PCE went from an estimated growth of 3.1% in Q1 to a growth rate of only 1.8% while GPDI was revised up from 0.5% during the second estimate to 5.0% during the third estimate.

The downward revision to PCE, which accounts for approximately 70% of GDP, changes this year’s trajectory for GDP growth, as the revision showed that what had been considered a strong consumer sector was significantly weaker than thought. It now appears that inflation had been taking much more out of real consumer demand than what the previous estimates were showing.

Furthermore, this week’s release of personal income and expenditures, with real disposable personal income down 0.1% in May after increasing 0.2% in April and real personal consumption expenditures at

-0.4% in May after increasing 0.3% in April puts the trajectory for consumer demand on an even weaker path than in Q1. Having said this, we still believe that personal consumption expenditures will remain positive in the second quarter. But the weakening in personal consumption expenditures is calling into question the staying power of the US consumer as well as the staying power of the savings accumulated during the COVID-19 pandemic.

What is in store for the Federal Reserve?

This week’s information could be a game-changer, again, for the Federal Reserve (Fed). The only thing that is still not certain is the path of inflation. The core PCE price deflator came down from 4.9% in April to 4.7% in May and if this year-over-year decline is sustained over the next several months, the Fed may not have to raise interest rates as high as markets are expecting today.

We still believe that July’s increase in the fed funds rate is going to be 75 bps but after that, the path seems less certain, especially if core PCE continues to slow down. Two weeks ago the higher than expected CPI plus the preliminary Michigan Survey five-year inflation expectations sent shivers into Fed officials and they decided to ‘up-the-ante’ This week’s revision to personal consumption expenditures growth during the first quarter of the year, even though it was ‘water under the bridge,’ puts consumer demand at a weakened pace compared to previous expectations. This means that there is a real possibility that inflation numbers during the second half of the year could come down at a faster pace than markets were expecting before.

This also means that current monetary policy (plus inflation) has been very effective in slowing down consumption and could prompt Fed officials to be more patient with their future rate increases because the economy is on a clear slowing path.

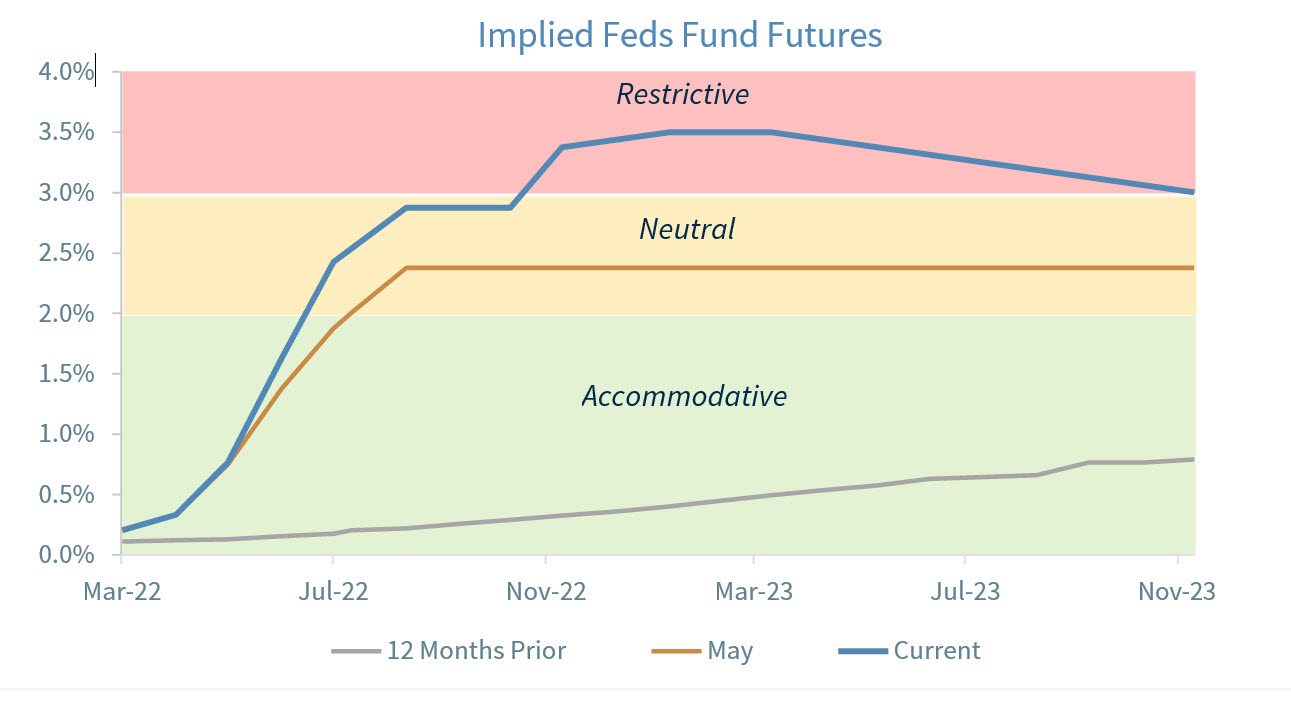

For the last twelve months until earlier this year, we expected the Fed to remain accommodative to help the economy ‘accelerate’ its way back to its pre-pandemic levels. However, as inflation started to increase significantly, we changed our view to a more ‘Neutral’ Fed, which is where interest rates are consistent with the Fed’s dual mandate of full employment and price stability. At the time we believed a moderate increase in rates would have sufficed with inflation peaking by March, on a year earlier basis. However, the sudden increase in oil (gasoline) and food prices brought about by the Ukraine-Russia conflict changed the whole inflationary path. By June, the Fed changed its tone and went into a more aggressive posturing with a 75 basis points hike after a worse-than-expected CPI reading and five-year inflation expectations moving higher than expected. With this fast change of heart, the Fed is expected to continue to raise rates likely to a ‘Restrictive’ level, which will put further pressure on the economy. Currently, we don’t expect the Fed to have to raise rates as high as the FOMC projections of 3.8%, but if inflation doesn’t improve quickly, it will likely have to move into the ‘Restrictive’ territory.

Economic and market conditions are subject to change.

Opinions are those of Investment Strategy and not necessarily those Raymond James and are subject to change without notice the information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. There is no assurance any of the trends mentioned will continue or forecasts will occur last performance may not be indicative of future results.

Consumer Price Index is a measure of inflation compiled by the US Bureau of Labor Studies. Currencies investing are generally considered speculative because of the significant potential for investment loss. Their markets are likely to be volatile and there may be sharp price fluctuations even during periods when prices overall are rising.

Consumer Sentiment is a consumer confidence index published monthly by the University of Michigan. The index is normalized to have a value of 100 in the first quarter of 1966. Each month at least 500 telephone interviews are conducted of a contiguous United States sample.

The producer price index is a price index that measures the average changes in prices received by domestic producers for their output. Its importance is being undermined by the steady decline in manufactured goods as a share of spending.

Industrial production: Industrial and production engineering is a measure of output of the industrial sector of the economy. The industrial sector includes manufacturing, mining, and utilities.

Personal Consumption Expenditures Price Index (PCE): The PCE is a measure of the prices that people living in the United States, or those buying on their behalf, pay for goods and services. The change in the PCE price index is known for capturing inflation (or deflation) across a wide range of consumer expenses and reflecting changes in consumer behavior.

FHFA house price index is a quarterly index that measures average changes in housing prices based on sales or refinancing’s of single-family homes whose mortgages have been purchased or securitized by Fannie Mae or Freddie Mac.

Consumer confidence index is an economic indicator published by various organizations in several countries. In simple terms, increased consumer confidence indicates economic growth in which consumers are spending money, indicating higher consumption.

ISM Manufacturing indexes are economic indicators derived from monthly surveys of private sector companies.

ISM Services Index is an economic index based on surveys of more than 400 non-manufacturing (or services) firms’ purchasing and supply executives.

Non-Manufacturing Business Activity Index is a seasonally adjusted index released by the Institute for Supply Management measuring business activity and conditions in the United States service economy as part of the Non-Manufacturing ISM Report on Business.

New orders index measures the value of the orders received in the course of the month by French companies with over 20 employees in the manufacturing industries working on orders.

Source: FactSet, data as of 6/3/2022