The Economy, Trade Policy, and Other Things

Chief Economist Scott Brown discusses current economic conditions.

Financial market participants have generally reacted little to economic data reports over the last several months. On a daily basis, the two key drivers have been trade policy and the Fed, and that’s expected to continue for the foreseeable future. However, tensions in Washington have escalated and are about as bad as they can get. The financial markets weren’t much perturbed by developments, but that may change.

The economic data reports have remained mixed, suggesting moderate growth in consumer spending, but general weakness in business investment. That pattern is expected to continue in the near term. Inflation-adjusted, consumer spending, 68% of Gross Domestic Product, rose just 0.1% in August, but that followed a 2.0% gain over the five previous months (a 4.7% annual rate). The strength in spring and early summer followed weakness at the end of last year and into the early part of 2019. Consumer spending growth is rarely smooth over time, but the year- over-year pace (+2.3%) is moderately strong. Spending is expected to remain supported by solid fundamentals (job gains and wage growth). The Conference Board’s Consumer Confidence Index fell sharply in the initial estimate for September, but we saw a similar dip amid rising trade tensions in June. What will keep consumers from spending? It’s simple. Take away their jobs. Job growth has slowed this year, but has remained well above a pace needed to absorb new entrants into the workforce. Announced corporate layoff intentions rose 36% in the first eight months of 2019 (relative to the same eight months in 2018), but the level has remained very low by historical standards.

Trade policy appears to be having a bigger impact on the economy. Looking ahead to next year, firms report a lack of visibility on pricing and the ability to import goods and supplies from China. As Fed Chair Powell noted in his September 18 press conference, “Our business contacts around the country have been telling us that uncertainty about trade policy has discouraged them from investing in their businesses.” The likelihood of a complete deal resolving trade tensions between the U.S. and China appears remote, but there is hope for a mini deal, one that would prevent a further escalation in trade tensions (and possibly de-escalate somewhat). The stock market has reacted to the one-step-forward-one-step- backward pattern in trade policy and we are likely to see an increased sensitivity as trade talks resume this month.

Meanwhile, the other major factor for the markets has been Fed policy. Chair Powell has noted that the Fed has no experience with a trade war. The last major conflict was during the Great Depression. The Fed does pay close attention to the economic data and the information gleaned from talking to businesses around the country. The Fed cut short-term interest rates in late July and mid-September, citing the impact from trade policy uncertainty and slower global growth, the downside risks these factors posed, and the low trend in inflation. Inflation has ticked up slightly (the year-over-year increase in the core PCE Price Index rose to 1.8% in August, still below the Fed’s 2% goal, but closer). Trade tensions have continued and geopolitical risks (such as Brexit) are more immediate. While Fed officials have been split on whether further rate cuts will be needed, the balance of power on the Federal Open Market Committee tilts toward more accommodation – but the correct answer on Fed policy is always “it depends.”

Last week, the financial markets were not particularly perturbed by the developments in Washington. The prevailing market view is that, after all, even if the House votes to impeach (only a simple majority is needed), the Senate (at this point) appears unlikely to amass the two-thirds majority needed to remove President Trump from office. President Clinton was impeached and the Senate failed to convict, and the stock market held up pretty well. Moreover, impeachment backfired against the Republicans, as they lost seats in the 1998 election.

Fear of a possible backlash may have been a key factor preventing House Speaker Pelosi from starting impeachment proceedings earlier, but there was another important reason. Nothing else is going to get done now (not that much was being done in the Senate anyway). The fiscal year begins on October 1. Congress is set to approve a Continuing Resolution to fund the government through mid-November, but we’ll eventually need a completed budget for FY20. There is a risk of a government shutdown, but that did not go so well last time (recall that we started the year with increased uncertainty and weakness in consumer spending). By itself, a lengthy impeachment process would add to business uncertainty, further dampening capital expenditures and perhaps new hiring.

Needless to say, there is a potential for significant financial market turmoil here. As is well known, the market often climbs a wall of worry, but sometimes the wall wins. The critical issue for the economic outlook will be the job market. Given the proximity to the zero lower bound, any sign of deterioration in the labor market would likely lead to a quick and aggressive response from the Fed. It’s unlikely that we’ll see such a deterioration in the near term, but it would be wise to keep an eye on things.

Data Recap – The economic data were mixed and had little impact on the financial markets. Investors remained focused on the prospects for trade talks and generally ignored developments in Washington.

House Democrats launched Impeachment Proceedings following a whistleblower’s complaint that President Trump sought foreign help in undermining a political opponent and the White House tried to cover it up. As a reminder, the House of Representatives can impeach the president with a simple majority vote. The Senate would then put the president on trial, where a two-thirds majority is needed for removal from office. The House has voted to impeach two presidents, Andrew Johnson and Bill Clinton, but both were acquitted in the Senate. Richard Nixon resigned as impeachment proceeding were underway.

Real GDP rose at a 2.0% annual rate in the 3rd estimate for 2Q19 (vs. 2.0% in the 2nd estimate). Consumer Spending rose at a 4.6% pace (vs. +4.7% in the second estimate), following two soft quarters. Business fixed investment fell 1.0% (vs. -0.6%). Residential fixed investment fell 3.0%, the sixth consecutive quarterly decline (although expected to be up in 3Q19).

Personal Income rose 0.4% in August (+4.6% y/y), led by a 0.7% increase in aggregate private-sector wages and salaries (+5.8% y/y). Farm income fell 5.7% (+13.7% y/y, supported by subsidies). Interest income slipped 0.6% (-0.2% y/y), while dividend income rose 0.4% (+3.4% y/y). Personal Spending rose 0.1% (+3.7% y/y), also up 0.1% (+2.3% y/y) adjusted for inflation. The PCE Price Index was unchanged (+0.033% before seasonal adjustment, +1.4% y/y), up 0.1% ex-food & energy (+0.140% before rounding, +1.8% y/y, vs. the Fed’s goal of 2.0%).

The Consumer Confidence Index dropped to 125.1 in the initial estimate for September, vs. 134.1 in July. The Conference Board noted that “the escalation in trade and tariff tensions in late August appears to have rattled consumers.” The drop appears to reflect increased concerns about tariffs. We saw a similar decline amid trade tensions in June. The year-over-year change in the present conditions index fell to -0.4 (a negative figure has often preceded past recessions). While less ecstatic than in August, job market perceptions remained relatively strong. Respondents were less optimistic about future business conditions, job availability, and income prospects.

The University of Michigan’s Consumer Sentiment Index edged up to 93.2 in the full-month assessment for September, vs. 92.0 at mid-month and 89.8 in August.

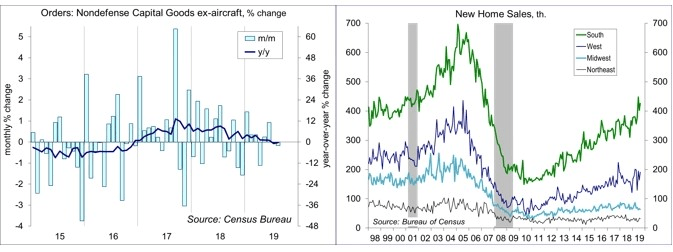

Durable Goods Orders rose 0.2% in the initial estimate for August. Transportation orders were mixed, falling 0.4% (motor vehicles -0.8%, civilian aircraft -17.1%, defense aircraft +30.3%). Ex-transportation, orders rose 0.5%, following a 0.5% decline in July. Orders for nondefense capital goods ex-aircraft fell 0.2%, up 1.1% y/y for the first eight months of 2019. Shipments for this category rose 0.4%, following a 0.6% decline in July. Ex-transportation, unfilled orders edged up 0.1% (+0.8% y/y). Inventories rose 0.3% (+5.2% y/y), down 0.1% excluding transportation (+2.3% y/y).

New Home Sales jumped 7.1% (±20.3%) in August, to a 713,000 seasonal adjusted annual rate up 18.0% (±19.9%) y/y. Sales were mixed across regions. Unadjusted sales for June-August were up 15.5% y/y (Northeast -11.1%, Midwest -5.6%, South +24.1%, West +14.6%).

The Pending Home Sales Index rose 1.6% in August, vs. -2.5% in July (+2.5% y/y). The monthly figures are choppy, but the underlying trend appears to be picking up.

The Chicago Fed National Activity Index rose to +0.10 in the initial estimate or August. At -0.06, the three month average was consistent with slightly below-trend growth in the overall economy in the near term.

The opinions offered by Dr. Brown should be considered a part of your overall decision-making process. For more information about this report – to discuss how this outlook may affect your personal situation and/or to learn how this insight may be incorporated into your investment strategy – please contact your financial advisor or use the convenient Office Locator to find our office(s) nearest you today.

All expressions of opinion reflect the judgment of the Research Department of Raymond James & Associates (RJA) at this date and are subject to change. Information has been obtained from sources considered reliable, but we do not guarantee that the foregoing report is accurate or complete. Other departments of RJA may have information which is not available to the Research Department about companies mentioned in this report. RJA or its affiliates may execute transactions in the securities mentioned in this report which may not be consistent with the report’s conclusions. RJA may perform investment banking or other services for, or solicit investment banking business from, any company mentioned in this report. For institutional clients of the European Economic Area (EEA): This document (and any attachments or exhibits hereto) is intended only for EEA Institutional Clients or others to whom it may lawfully be submitted. There is no assurance that any of the trends mentioned will continue in the future. Past performance is not indicative of future results.