The income is back in fixed income

Doug Drabik discusses fixed income market conditions and offers insight for bond investors.

Sometimes a picture is indeed worth a thousand words. The Treasury market has plunged during the month of August raising two year and five year interest rates 62 and 72 basis points respectively. Treasury yields are well over 3.00% and when you look at investment-grade fixed income products, income buyers can get excited about the yields they can lock into their portfolios. Now is proving to be one of the most promising periods of time in decades to boost portfolio income with your portfolio’s fixed income allocation.

Here are two of the more popular requests we are discussing with income buyers:

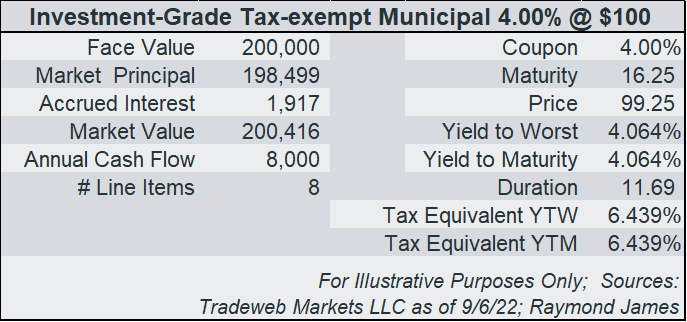

Investors seeking to lock in strong yields with tax-exempt income are taking advantage of 4.00% coupon municipal bonds now priced around par. In this illustration, 4.00% coupon municipal bonds were laddered from 2035 to 2042 to average an 11.69 duration with a yield-to-worst of 4.064%. For investors in the highest tax bracket, that is a 6.439% taxable equivalent yield.

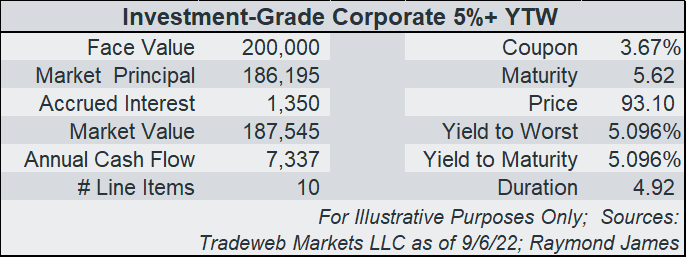

Another popular request has been to maximize yield in the sweet spot of the curve. Investors in investment-grade corporate bonds are able to realize +5% yields. In this illustration, corporate bonds were laddered with maturities from 2026 to 2030. The income investor is able to average a 5.096% yield using bonds priced at a discount.

Although these two illustrations are among the more frequent requests, increased yields are presenting opportunities in a variety of fixed income product types and in strategies that can be tailored to specific investor biases, needs, risk profiles and goals. I encourage you to talk with your financial advisor to discuss the numerous fixed income opportunities as well as the specifics of individual bonds. Now is proving to be a moment in time when fixed income can provide increased income. Investors can counter the overall market’s uncertainty with known cash flow and income certainty.

The author of this material is a Trader in the Fixed Income Department of Raymond James & Associates (RJA), and is not an Analyst. Any opinions expressed may differ from opinions expressed by other departments of RJA, including our Equity Research Department, and are subject to change without notice. The data and information contained herein was obtained from sources considered to be reliable, but RJA does not guarantee its accuracy and/or completeness. Neither the information nor any opinions expressed constitute a solicitation for the purchase or sale of any security referred to herein. This material may include analysis of sectors, securities and/or derivatives that RJA may have positions, long or short, held proprietarily. RJA or its affiliates may execute transactions which may not be consistent with the report’s conclusions. RJA may also have performed investment banking services for the issuers of such securities. Investors should discuss the risks inherent in bonds with their Raymond James Financial Advisor. Risks include, but are not limited to, changes in interest rates, liquidity, credit quality, volatility, and duration. Past performance is no assurance of future results.

Investment products are: not deposits, not FDIC/NCUA insured, not insured by any government agency, not bank guaranteed, subject to risk and may lose value.

To learn more about the risks and rewards of investing in fixed income, access the Securities Industry and Financial Markets Association’s Project Invested website and Investor Guides at www.projectinvested.com/category/investor-guides, FINRA’s Investor section of finra.org, and the Municipal Securities Rulemaking Board’s (MSRB) Electronic Municipal Market Access System (EMMA) at emma.msrb.org.